The latest UBS Global Real Estate Bubble Index 2023 has just been released, here are my key takeaways.

Dubai has once again been classed as ‘fair valued’ and is mostly due too supply and demand, cost of living, cash purchases, payment plans as opposed to financed properties, and income.

‘Low financing costs have been the lifeblood of global housing markets over the past decade, driving home prices to dizzying heights. However, the abrupt end of the low-interest rate environment has shaken the house of cards. On average of all cities, within the past year, inflation-adjusted home prices have seen the sharpest drop since the global financial crisis in 2008.’

Dubai in the safety zone – Fair Valued

‘The sharpest rises in rents were recorded in Singapore and Dubai.’

/With housing prices sliding for seven straight years, the market for owner-occupied housing in Dubai started recovering in 2021. The risk score has dropped significantly over the course of this 10-year period. In the last four quarters, housing prices increased by a double-digit rate. Given strong income growth and a red-hot rental market, with rental growth even surpassing owner-occupied price growth, we see the market as fairly valued. While Dubai is highly cyclical and prone to overbuilding, price momentum should remain strong in the coming quarters/

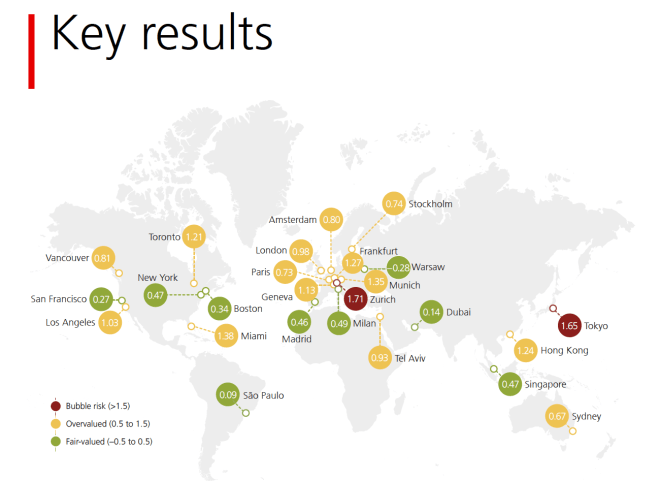

Dubai

‘The seven-year long drought of falling real estate prices has become a distant memory. Prices have been booming since 2021 and increased by 15% in inflation-adjusted terms between mid-2022 and mid-2023, the highest growth rate among all cities analyzed in the study. Price increases in the luxury segment were even stronger.

Dubai has attracted real estate investors globally. A new visa program with looser residency requirements aimed at wealthy and skilled individuals, no personal income tax, and early lifting of travel restrictions during the pandemic have stimulated immigration. Moreover, supported by higher commodity prices, Dubai has seen strong economic and household income growth since 2021, topping other cities. Consequently, residential transaction volumes have gone through the roof, breaking all-time highs. Nevertheless, inflation-adjusted prices are around 25% below their 2014 peak. Furthermore, as many newcomers rent before potentially buying in the future, rents have increased by 20% in inflation-adjusted terms over the last four quarters. As a result, the market remains in fair value territory, in our view.

We expect weakening momentum in the coming quarters. Although the market is largely financed by cash purchases, increased mortgage interest rates will take their toll. An ongoing strong expansion of supply—particularly of apartments—is also likely to limit price growth.’

Identifying a bubble

Price bubbles are a recurring phenomenon in property markets. The term “bubble” refers to a substantial and sustained mispricing of an asset, the existence of which cannot be proved unless it bursts. But historical data reveals patterns of property market excesses. Typical signs include a decoupling of prices from local incomes and rents, and imbalances in the real economy, such as excessive lending and construction activity. The UBS Global Real Estate Bubble Index gauges the risk of a property bubble on the basis of such patterns. The index does not predict whether and when a correction will set in. A change in macroeconomic momentum, a shift in investor sentiment or a major supply increase could trigger a decline in house prices.